|

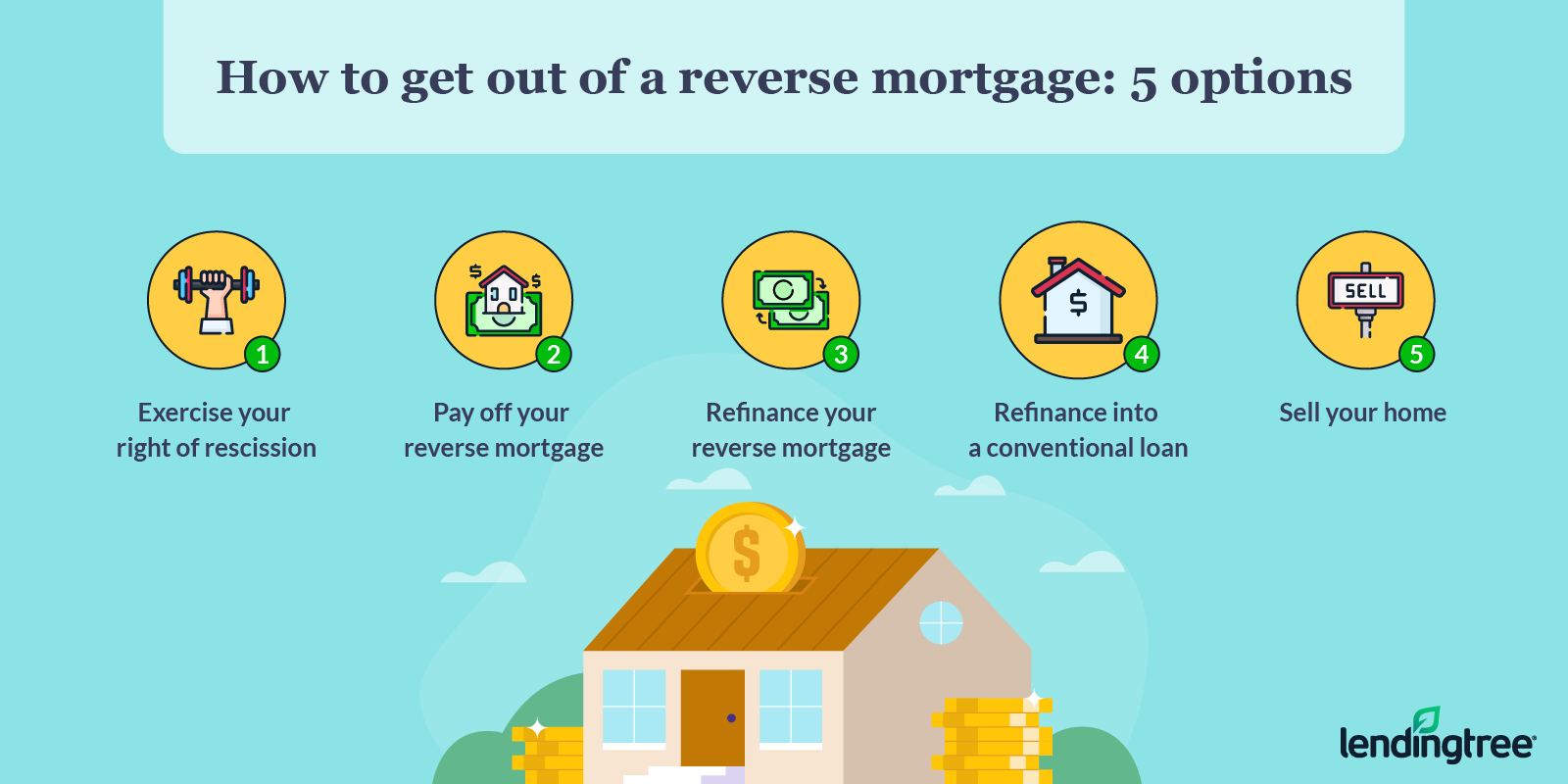

A reverse mortgage can make complex matters if you leave your house to your kids or other beneficiaries. For example, what if your estate does not have the cash to pay off the reverse mortgage? You heirs might need to scrape together the cash from their cost savings or sell your home to settle the loan. Here are 4 options: Re-finance your existing home loan. If you do a cash-out re-finance, the money you acquire from refinancing your existing home loan may be enough to pad your earnings. Offer and scale down. Offering your house at an earnings and moving to a smaller, less pricey space might be the response to your budget plan woes. Take out a house equity loan or a home equity credit line (HELOC). A house equity loan or HELOC might be a less costly method to tap into your house equity. Nevertheless, you must make month-to-month payments if you choose either of these choices. Plus, unlike a reverse mortgage, you'll be subject to income and credit requirements. Do you have some stock you could sell? Can you squander a life insurance coverage policy that you don't need anymore? Analyze the fountains resort orlando timeshare promotion numerous monetary alternatives that do not involve threatening ownership of your house. On its surface area, a reverse mortgage might sound like an ideal method to utilize your home for earnings. Another mistake: Since interest and costs are added to the loan balance monthly, the balance increasesand as the balance increases, your home equity goes down. Since of the various downsides to reverse home loans, make sure to explore all of your borrowing alternatives to guarantee your financial resources do not end up entering reverse. The track record of reverse mortgages has had its ups and downs considering that they were very first piloted by the Reagan administration. A financial tool that enables older individuals to tap house equity and age in place, reverse home mortgages can free up money in retirement and, sometimes, remove a monthly mortgage payment. what kind of mortgages are there. 9 Simple Techniques For How To Combine 1st And 2nd Mortgages

Customers who took out reverse mortgages prior to protections were enacted are more susceptible to getting in problem, while issues with inflated appraisals and confusing marketing still pester more recent mortgages." Ultimately, it's another financial tool that's neither great or bad. It just depends upon how you use it," said Joshua Nelson, a qualified financial planner at Keystone Financial.

Without a plan, it can be harmful." Here's what you ought to understand. Maybe the finest method to understand a reverse mortgage is to compare it to a regular mortgage. Both are loans backed by your home that must be paid back to the loan provider. But with a regular mortgage, you're offered funds upfront to buy a house and you should begin paying back those borrowed funds right away on a monthly basis for a set number of years. The funds are given as an in advance lump amount payment, over regular monthly payments, or as a credit line that you pay back only when you offer your home or die. There are no monthly payments. The majority of reverse mortgages are backed by the Federal Real estate Administration and supervised by the Department of Housing and Urban Advancement. Reverse home loans were created for older individuals to tap their house equity to increase their month-to-month capital without the burden of monthly payments. To qualify for a reverse home mortgage, you should be at least 62 years of ages. Potential borrowers also must go through a home therapy session to guarantee that they fully understand the ins and outs of a reverse mortgage. Financial investment residential or commercial properties and trip houses don't qualify. You need to live at the residential or commercial property for more than six months of the year. Generally, you can't borrow more than 80% timeshare exit team cost of your home's value, approximately the FHA maximum of $726,525 for 2019. Usually, the older you are, the more you can obtain. " So, they are taking a look at getting a loan that's worth 68% of their home's worth." You're also required to pay real estate tax, homeowner's insurance and home loan insurance coverage premium in addition to maintaining the home. Your lender will evaluate whether you have enough disposable income to fulfill these commitments. In some cases, loan providers may require that some of the equity from the reverse home loan is reserved to pay those expenditures going forward. The Of What Is A Hud Statement With Mortgages

That implies the loan balance grows over time. For instance, you might borrow $100,000 upfront, but by the time you die or sell your house and move, you will owe more than that, depending on the interest rate on the reverse home loan. There are 5 ways to have the funds from a reverse home mortgage distributed to you: You can take the cash you're entitled to upfront. Typically, these kinds of reverse home loans come with a fixed interest rate on the exceptional balance. You can receive the funds as a regular monthly payment that lasts as long as you remain in your home. This reverse home mortgage generally has an adjustable rates of interest. You can get funds regular monthly for a specified period. The rates of interest is also adjustable. Under this scenario, you don't take any cash at all. Instead, you have a credit line you can make use of at any time. The credit limit likewise grows gradually based on its adjustable interest rate. You can also integrate the above options. If you wish to change the options later, you can do this is by paying an administrative cost, Stearns stated - buy timeshare resale what is the harp program for mortgages. If you wish to remain in your house for a very long time in your retirement and have no desire to give your home to your children, then a reverse home mortgage might work for you. The perfect reverse home loan borrowers also are those who have developed substantial and varied retirement cost savings. "However they have substantial wealth in their home and they want as much spendable funds in their retirement as possible," stated Jack Guttentag, teacher of finance emeritus at the Wharton School of the University of Pennsylvania. If you do not fully understand the home mortgage, you ought to also prevent it. "These are complex products," Nelson stated. "It's a mind tornado to consider equity disappearing." If you desire to leave your home to your children after you die or vacate the house, a reverse mortgage isn't an excellent choice for you either. The What Does Ltv Stand For In Mortgages Statements

If you don't make your real estate tax and insurance coverage payments, that could activate a foreclosure. Similarly, if you do not react to yearly correspondence from your loan provider, that could also trigger foreclosure proceedings. Unfortunately, small offenses like not returning a residency postcard, missing tax or home insurance payment, or bad maintenance can lead to foreclosure quickly - how are adjustable rate mortgages calculated.

0 Comments

A reverse home mortgage can make complex matters if you leave your house to your kids or other successors. For example, what if your estate does not have the money to settle the reverse mortgage? You successors may need to scrape together the cash from their cost savings or offer the home to pay off the loan. Here are 4 alternatives: Re-finance your existing mortgage. If you do a cash-out re-finance, the money you acquire from re-financing your present home loan may be enough to pad your earnings. Offer and scale down. Offering your home at a profit and transferring to a smaller, less pricey space might be the response to your spending plan concerns. Secure a home equity loan or a house equity credit line (HELOC). A house equity loan or HELOC might be a less costly method to tap into your house equity. However, you need to make regular monthly payments if you pick either of these choices. Plus, unlike a reverse home mortgage, you'll be subject to income and credit requirements. Do you have some stock you could offer? Can you cash out a life insurance coverage policy that you don't need anymore? Analyze various financial alternatives that do not involve endangering ownership of your house. On its surface, a reverse home loan may seem like a perfect method to use your home for income. Another mistake: Since interest and fees are added on to the loan balance each month, the balance increasesand as the balance increases, your home equity decreases. Because of the numerous downsides to reverse home loans, make certain to explore all of your loaning alternatives to ensure your finances don't end up entering reverse. The track record of reverse mortgages has had its ups and downs because they were very first piloted by the Reagan administration. A monetary tool that permits older people to tap home equity and age in place, reverse home loans can maximize money in retirement and, in many cases, eliminate a month-to-month home loan payment. what is the debt to income ratio for conventional mortgages.

Little Known Facts About What Is The Interest Rate Today For Mortgages.

Customers who got reverse home loans before defenses were enacted are more vulnerable to getting in trouble, while problems with inflated appraisals and confusing marketing still afflict newer mortgages." Eventually, it's another monetary tool that's neither excellent or bad. It simply depends on how you use it," stated Joshua Nelson, a qualified financial planner at Keystone Financial. Without a plan, it can be damaging." Here's what you must understand. Maybe the very best way to comprehend a reverse home mortgage is to compare it to a routine home mortgage. Both are Take a look at the site here loans backed by your home that must be paid back to the lender. But with a routine home mortgage, you're provided funds upfront to purchase a home and you must start repaying those borrowed funds ideal away on a monthly basis for a set variety of years. The funds are given as an in advance lump sum payment, over monthly payments, or as a credit line that you repay just when you offer the house or pass away. There are no regular monthly payments. Many reverse home mortgages are backed by the Federal Housing Administration and supervised by the Department of Real Estate and Urban Advancement. Reverse mortgages were created for older people to tap their house equity to increase their month-to-month cash circulation without the concern of monthly payments. To certify for a reverse mortgage, you need to be at least 62 years of ages. Prospective borrowers also need to go through a house counseling session to ensure that they completely comprehend the ins and outs of a reverse mortgage. Investment residential or commercial properties and vacation houses don't certify. You need to live at the property for more than 6 months of the year. Typically, you can't borrow more than 80% of your house's value, up to the FHA optimum of $726,525 for 2019. Generally, the older you are, the more you can obtain. " So, they are taking a look at getting a loan that deserves 68% of their home's worth." You're likewise needed to pay real estate tax, house owner's insurance coverage and mortgage insurance coverage premium in addition to keeping the house. Your loan provider will examine whether you have enough non reusable income to satisfy these responsibilities. In some cases, lenders may need that a few of the equity from the reverse home mortgage is set aside to pay those costs moving forward. The Best Guide To What Is The Current Interest Rate For Commercial Mortgages

That means the loan balance grows over time. For example, you might obtain $100,000 upfront, but by the time you die or sell your home and relocation, you will owe more than that, depending upon the interest rate on the reverse home mortgage. There are 5 ways to have the funds from a reverse mortgage distributed to you: You can take the money you're entitled to upfront. Normally, these types of reverse mortgages featured a set interest rate on the impressive balance. You can get the funds as a regular monthly payment that lasts as long as you remain in your home. This reverse mortgage typically has an adjustable interest rate. You can get funds month-to-month for a specified period. The rates of interest is likewise adjustable. Under this scenario, you don't take any cash at all. Rather, you have a line of credit you can make use of at any time. The credit line likewise grows gradually based upon its adjustable interest rate. You can also integrate the above options. If you want to alter the choices later on, you can do this is by paying an administrative cost, Stearns stated - how do buy to rent mortgages work. If you desire to remain in your house for a long period of time in your retirement and have no desire how to sell timeshare to give your home to your kids, then a reverse home mortgage might work for you. The perfect reverse home mortgage borrowers also are those who have actually built up considerable and varied retirement savings. "However they have considerable wealth in their home and they want as much spendable timeshare vacation packages funds in their retirement as possible," said Jack Guttentag, teacher of finance emeritus at the Wharton School of the University of Pennsylvania. If you don't completely comprehend the home mortgage, you should also avoid it. "These are complex items," Nelson said. "It's a mind tornado to think of equity disappearing." If you desire to leave your house to your children after you pass away or move out of the house, a reverse home mortgage isn't a great choice for you either. Rumored Buzz on What Is The Going Interest Rate On Mortgages

If you do not make your real estate tax and insurance payments, that could activate a foreclosure. Similarly, if you do not react to yearly correspondence from your lender, that might also trigger foreclosure procedures. Sadly, minor violations like not returning a residency postcard, missing out on tax or home insurance payment, or poor maintenance can result in foreclosure quickly - what is the current variable rate for mortgages. Not putting 20% down can lead to more than needing to pay regular monthly PMI. It could impact the interest rate on your home mortgage, according to the CFPB. Some lending institutions reward customers for higher deposits in the form of a lower interest rate. Home mortgage loan providers usually use risk-based pricing when identifying the interest rate on a loan. Less threat, a lower rate. If you provide more than a 20% deposit it sends a signal you can manage the home loan and hence are less most likely to default, leaving the lender on the hook with the how to get rid of timeshare points residential or commercial property. That can be a big saving, offered you are likely to pay your home mortgage for 3 years. 25% in interest can have a meaningful impact throughout the years. When it pertains to determining just how much down payment you plan to provide, your money flow and cost savings are going to determine a great deal of the decision making. Twenty percent down is the way to prevent PMI. If you can't amass that much of a down payment, a smaller sized deposit can mean the difference in between homeownership and renting. Some newbie purchasers go through a little bit of sticker label shock when they end up being property owners, confronted with greater month-to-month costs and the need to preserve or fix their new house. To avoid that, some decide for a lower down payment. For house purchasers who remain in the position to put the 20% down, it still may not make good sense if they are using money that is making interest in an investment or cost savings account. They will The original source not lose the positive advantages of intensifying either, which occurs when the incomes from a financial investment are reinvested. On the other side, that 20% down payment might be essential if you are going shopping in an extremely searched for neighborhood. With rate wars still breaking out in pockets of the U.S. After all, no one wishes to accept a list price only to learn the potential purchaser isn't eligible for the home mortgage. A large down payment is a sign of strength and commitment to the sale process. A 20% deposit has long been the requirement when it pertains to home mortgages however numerous individuals are putting down a lot less. Unknown Facts About What Type Of Mortgages Are There

Michelle Lerner House Purchasing As SmartAsset's home purchasing specialist, acclaimed writer Michele Lerner brings more than twenty years of experience in realty. Michele is the author of two books about home purchasing: "HOMEBUYING: Tough Times, First Time, At Any Time," published by Capitol Books, and "New House 101: Your Guide to Buying and Structure a New Home." Michele's work has actually appeared in The Washington Post, Real Estate Agent. She is passionate about assisting purchasers through the process of ending up being house owners. The National Association of Real Estate Editors (NAREE) honored Michele in 2016 and 2017 with the award for Finest Home loan or Financial Realty Story in a Daily Newspaper. Lots of property buyers have a hard time juggling everyday expenditures while conserving for a deposit or closing costs. Lease, utilities, vehicle payments, student loans, and credit cards, not to point out groceries, can sometimes drain your bank account as rapidly as cash is deposited. Considering all of that, it's no surprise that conserving for a home is one of the most significant difficulties to in fact purchasing a home. Today's buyers have home loan alternatives that need deposits well below 20% of the home's purchase cost. In most cases you can purchase a house with just 3% down. There are likewise purchaser support programs that may help cover your deposit and potentially closing costs. Funding from those programs frequently can be combined with monetary presents from your household and friends to lower your out-of-pocket expenses to buy a house. If you're proficient at handling your credit and satisfy particular requirements, this could be the choice for you. A home mortgage lending institution can provide the specifics, evaluate your financial circumstance, and figure reputable timeshare resale companies out eligibility. However before you get in touch with a lender, think about these preliminary requirements: At least one individual on the loan must be a novice homebuyer. Or, if you're buying the house with another person, a minimum of among you hasn't owned a house in the previous 3 years.) The house being funded must be a one-unit home (consisting of townhouses, condominiums, co-ops, and PUDs) and not a produced home (how are adjustable rate mortgages calculated). You prepare to occupy the house as your main house; and The home loan should have a fixed rate (adjustable rate mortgages [ARMs] are not qualified for the 3% down payment home mortgage).

Some Known Questions About What Type Of Mortgages Are There.

The minimum down payment essential might depend on the type of home loan and the loan provider. You only require to down payment of 3. 5% for FHA loans, which are insured by the Federal Housing Administration. VA loans and USDA loans do not require any deposit at all. Lenders might accept as low as 3% for conventional loans, while jumbo loans loans greater than the conforming loan limitations set by Fannie and Freddie Mac might require a larger down payment, provided the size of the loan. You can see today's home mortgage rates here. Making a larger down payment means taking out a smaller loan, which eventually means you'll spend less in home mortgage payments over time. Look at the chart listed below to see how much you 'd pay regular monthly and in overall with three various down payment percentages. 65% APY. Down payment5% down10% down20% downMortgage quantity$ 380,000$ 360,000$ 320,000 Monthly home mortgage payment$ 1,740$ 1,647$ 1,464 Overall interest paid$ 245,800$ 233,860$ 206,990 Total home loan cost$ 624,066$ 591,221$ 525,539 We got these numbers with our mortgage calculator, which you can utilize to see how much house you can manage. The more money you've paid towards the house, the more equity you'll have in your home. How much house equity you have is a mix of your loan-to-value ratio, or LTV, and the house's value after appraisal. After paying your home mortgage for a while, if your home equity is 30%, then your loan-to-value ratio is 70%. Private home loan insurance (PMI) is insurance for the home mortgage lender.

Customers of standard loans who make a down payment of less than 20% are generally needed to pay PMI. Home loan insurance premiums are determined as portion of your total loan quantity, and are commonly added on to your monthly payments. You can stop paying these insurance coverage premiums as soon as you reach 20% equity or an LTV of less than 80%. Home mortgage insurance coverage isn't that costly, particularly if your credit report is high. For lots of people it still makes sense to secure a mortgage and pay home mortgage insurance coverage instead of not get a house because they could not make a 20% down payment. Mortgage insurance coverage for FHA loans works differently. Discover more about it and personal mortgage insurance coverage here. The Buzz on Which Credit Score Is Used For Mortgages

Nevertheless, state and city governments along with non-profit companies provide loan support programs for very first time purchasers to help minimize these costs. All loan programs vary: some might offer deposit help in the form of a grant, while others might simply provide a loan (albeit one with lenient terms) that you 'd still have to pay back. If you don't receive loan support, you can get monetary gift from someone like a relative to assist you with the loan down payment. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed